The United Nations General Assembly promoted the publication of seventeen Sustainable Development Goals (SDGs) to deal with the massive global economic, social and environmental challenges and uncertainties the world is facing, which require unprecedented and cohesive actions from citizens, governments and organizations.

In this context, organizations have to face the challenge of turning policies into action and take a more consistent approach to sustainable issues by conducting robust impact assessment and reporting their performances. They are expected to provide insightful information beyond their annual key financial data, with the aim of offering an account of their ongoing attempts made to integrate competitive strategies and SDGs.

Integrated reporting represents a promising approach to disclose organizations’ journey towards the integration of SDGs within their business models.

Among the most diffused accounting and reporting practices, integrated reporting (IR) represents a promising approach to disclose organizations’ journey towards the integration of SDGs within their business models. Developed and promoted by the International Integrated Reporting Council (IIRC), it is based on the connectivity and interdependencies between a range of capitals (financial, manufacturing, human, intellectual, social and relationship, and natural) that affect an organization’s ability to create value and be sustainable. In particular, IR funds its basis on the concept of Integrated Thinking and aims at offering an engagement platform to support companies in addressing and delivering SDGs by facilitating the alignment of strategy and business model with sustainable development issues.

Integrating SDGs into reporting processes: the cases of PepsiCo and City Developments Limited

The experience of PepsiCo and City Developments Limited illustrates how IR and SDGs can support organizations in defining risks, prioritizing activities and developing clear and successful strategies for better and more holistic approaches to sustainable development and value creation.

The case of PepsiCo: mapping corporate strategy with the SDGs

PepsiCo is an American leader in the food and beverage industry that sells products in more than 200 countries. PepsiCo’s attention to sustainable development started in 2006 when the company launched its ‘Performance with Purpose’ (PwP) strategy, aimed at expanding the organization’s portfolio of more nutritious products, shrinking their environmental footprint, acting as a good global citizen and working to improve employees’ and their families’ working and living conditions (See Figure 1).

More recently, the company decided to align its PwP strategy with the most relevant SDGs impacted by its traditional activities. In particular, PepsiCo’s integrated Sustainability Report 2017 identified, for each of the three key strategic goals, the seven SDGs it directly impacts and provided examples of the actions implemented in the company’s daily activities (see Figure 2).

The case of City Developments Limited: determining the connectivity between capitals and SDGs

City Developments Limited (CDL) is a multinational real estate company listed on the Singapore Stock Exchange. It operates in more than 100 locations and 28 countries around the world. Its investment portfolio comprises residences, offices, hotels, serviced apartments and shopping malls, totalling over 18 million square feet of floor area globally.

In 2015, CDL was one of the first organizations in Singapore that developed an integrated report. Further, in 2017, the organization promoted a sustainability blueprint guide labelled CDL Future Value 2030. It is based on the six capitals promoted by the IIRC Framework and is also aligned with 13 of the 17 SDGs promoted by the United Nations. In particular, the CDL blueprint aims to:

- Communicate to internal and external stakeholders how the organization is operating to address the fast-changing environmental and business landscape by making ESG performance financially measurable;

- Reinforce CDL’s established sustainability strategy and best practices in creating value for business, investors, stakeholders, community and the planet;

- Set out directions and ESG guidelines to CDL’s business and stakeholders;

- Define CDL’s position as a sustainable leader in the real estate management and development sector.

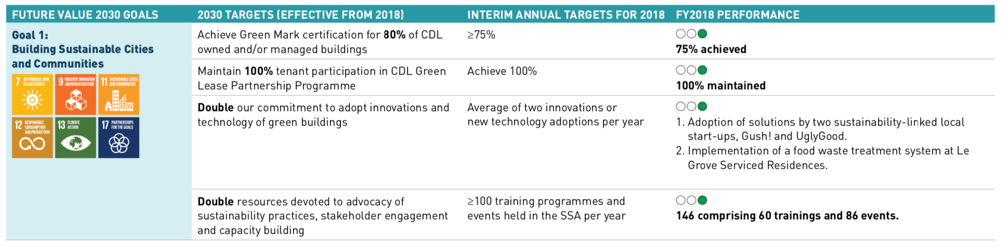

In accordance with CDL’s key strategic goals – respectively Building on sustainable cities; Reducing environmental impact; Ensuring Fair, Safe and Inclusive Workplace -, the blueprint provides information on the actions taken by the organization during the year (i.e., 2018) to address the ESG dimension, and the operations planned to contribute to the UN’s SDGs by 2030.

As shown in Figure 3, CDL’s strategic goals are monitored annually according to the actual performance achieved (in 2019) and their variation from past and future targets. Figure 4 also shows the SDGs impacted by each of the organization’s performances and targets.

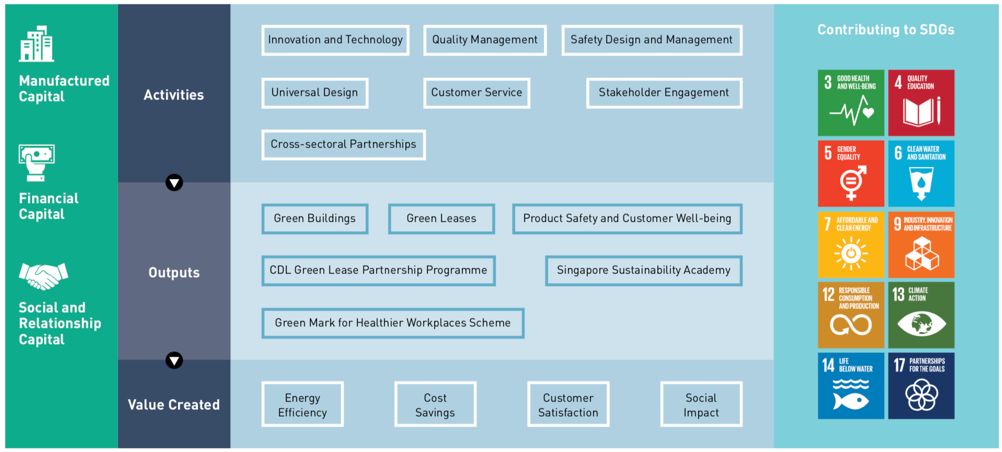

To further highlight the correlation between organization strategies, actions, performance and SDGs, the CDL’s 2019 integrated report provides a new step of disclosure by integrating capitals, past performances, specific targets and sustainable development goals within the same table.

Interestingly, the table in Figure 4 illustrates how the key capitals exploited throughout the organization’s value-creation process impact on the most material SDGs. It also highlights the activities and initiatives performed, the output achieved, and the value created for the business and its stakeholders.

Nurturing the interconnections between SDGs and IR

As shown by the analysis of these case studies, integrating SDGs into business models and strategic objectives can allow organizations to offer useful insights to investors in addressing their concerns, improve financial and non-financial risk mitigation processes, and raise awareness of the importance of sustainable development in the long-term. In particular, to effectively manage the integration of SDGs and long-term strategic objectives, a company would need to:

- Secure the understanding, interest, and commitment of high-profile leaders who are willing to champion the adoption of the SDGs;

- Map and prioritize the SDGs relevant to the organization’s business model and incorporate the SDGs into its strategy;

- Design a system of alignment between capitals and SDGs and define their reciprocal impacts within the business model;

- Create a cross-functional work group to ensure engagement, diversity, and inclusiveness while the concept of integration is being applied to planning, measurement, and reporting;

- Clarify the difference between performing sustainability and sustainable performance(s) early in the process, and bring the finance sector on-board, together with other organizational functions;

- Focus on the intrinsic purpose of a business and on the multiple objectives to be achieved, considering the various stakeholders that an organization engages within the value chain;

- Understand the financial, operating and ESG objectives as well as the expected targets that are linked into the organization’s strategic plan;

- Identify the resources, the activities, the drivers, and the stakeholders involved in the development and execution of the business model;

- Recognize the trade-offs, interests and risks that characterize the value creation process – especially across and within the capitals and the SDGs;

- Share the achievements of the SDGs in order to regain society’s trust and secure the license to operate by working with governments, consumers, workers and civil society.

This way, both IR and SDGs can support organizations in defining risks, prioritizing activities, and developing clear and successful strategies for better and more holistic approaches to sustainable development and value creation.